STOCKS

33 Undervalued ASX Stocks For 2026

We share our outlook for different sectors in Australia and highlight opportunities in 2026.

New Morningstar research has revealed that the real estate, healthcare and technology sectors are undervalued (as of Mar 31, 2026), as surging oil prices and higher rates have reshuffled star ratings across our coverage.

We have identified several stocks trading at attractive prices, with certain names trading at discounts to their long-term intrinsic value of up to 40% or more as of 31 Mar 2026.

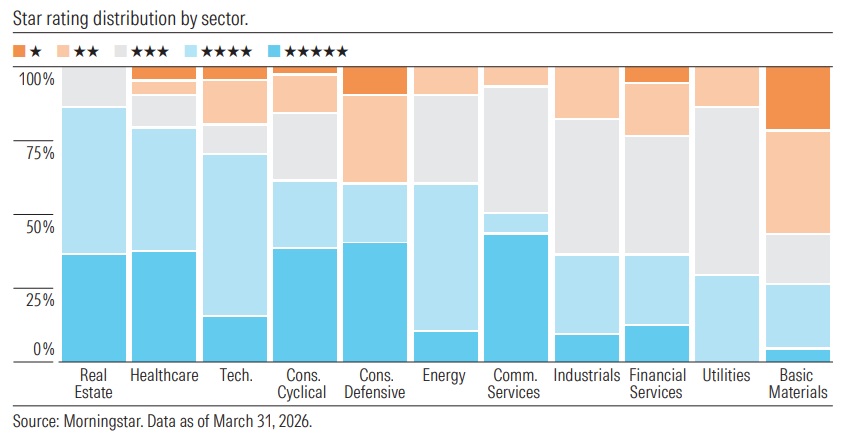

Morningstar valuation overview of Australian-listed firms under coverage as of 31 Mar 2026. 4- and 5-star ratings mean the stock is undervalued, while a 3-star rating means it's fairly valued, and 1- and 2-star stocks are overvalued.

Here’s a brief summary of how valuations stack up across sectors and where investors may find opportunities. Data is as of 31 March 2026.

Skip to sector:

- Energy

- Financial Services

- Technology

- Basic Materials

- Communication Services

- Consumer Cyclical

- Consumer Defensive

- Healthcare

- Industrials

- Real Estate

- Utilities

Energy

We maintain our USD 65 per barrel mid-cycle Brent crude price. Only in a remote probability scenario where an attack on Kharg Island knocks Iran's exports offline, or where Iran carries out an impassable structural block, might we change this input.

Kharg Island is responsible for 90% of Iran's exports, or 4.6 million barrels per day. Donald Trump has threatened to destroy this infrastructure if Iran continues to restrict shipping. It would be a meaningful bite of the global 104 million barrel per day demand.

But even in such a scenario, longer term, we still think Saudi Arabia and the United Arab Emirates have enough spare capacity to help drive prices back down to mid-cycle. A prolonged Iran conflict would likely only delay but not impair this outcome.

Futures prices, which we use for our next two year’s forecasts, have strengthened markedly, including by around 40% on average for Brent crude and by 75% for Asia spot LNG. Our year one and year two earnings forecasts for upstream oil and gas companies increase on average by 68% and 47%, respectively.

Undervalued stocks in the Energy sector

To see undervalued stocks in the energy sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX energy stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the energy sector currently trading at a 4- or 5- star rating.

Financial Services

Bank shares rallied on results, taking another leg up despite stretched valuations. Net interest margins held up, allowing strong credit growth and management of expenses to flow through to mid-single-digit profit growth. Shares are priced for much more than the five-year 6% EPS CAGR we forecast. Sentiment could change on higher interest rates to combat inflation, posing downside risks to credit growth and losses into fiscal 2027. Disruptions to supply chains and input costs from the Iran war could result in more bankruptcies without government intervention and could be a catalyst for higher unemployment. AI-related job losses are yet to move the employment needle but could drive bank loan losses back up to normalised levels in the medium term.

Given general insurance is commoditised, competition is eroding excess profits. Premium increases lagged claims inflation and higher natural hazard costs in first-half fiscal 2026. General insurers’ shares pulled back and are now more fairly valued.

Margins are likely to compress further across our wealth management coverage despite near-term profit momentum from strong net flows and rising FUM. Firms like Netwealth, Pinnacle, Generation Development, and L1 Group delivered solid profit growth in the last half, supported by adviser adoption, product enhancements, merger synergies, or share gains in higher-margin segments like private markets or ancillary platform fees. However, this is increasingly offset by reinvestment in distribution, technology, wages, and integration, which are eroding profit margins in several cases. While mix shifts and usage-based revenue provide some offset, we still expect moderated earnings growth ahead as cyclical fees normalise and competition endures.

Undervalued stocks in the Financial Services sector

To see undervalued stocks in the financial services sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX financial services stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the financial services sector currently trading at a 4- or 5- star rating.

Technology

The technology sector has materially underperformed the broader Australian market, down 45% from its August 2025 peak. We stressed then that prices were detaching from fundamentals, but the froth has unwound rapidly. Technology stocks were hit by a double whammy: fear AI renders software business models obsolete; and a hawkish domestic central bank that has already raised rates twice this year. We now view the sector as undervalued, near levels last seen in the aftermath of the late 2022 rate hikes.

Our approach is to remain disciplined, and we value companies based on discounted cash flows through the cycle. We do not expect AI to affect all software companies equally, and the indiscriminate sell-off is creating opportunities in high-quality names. Within our coverage, we see a resilient outlook for platforms embedded in complex, regulated workflows. We expect these businesses to incorporate AI into their product suites and capitalise on its lead over smaller competitors, rather than be displaced by it.

By contrast, we see greater risk of AI disruption for enterprise software providers that rely solely on switching costs. We believe lower development costs may enable larger players like SAP, or AI-native point solutions, to compete more effectively in its niche segments and erode pricing power.

Undervalued stocks in the Technology sector

To see undervalued stocks in the technology sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX technology stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the technology sector currently trading at a 4- or 5- star rating.

Basic Materials

The basic materials sector pulled back sharply recently on concerns the Iran war will push up oil prices, requiring central banks to raise interest rates to offset increasing inflation, slowing economic growth, and commodity demand. Even so, it is higher than last quarter on generally increased commodity prices and expensive on average. Gold is again stronger, by about 10%, after reaching yet another historical high of about USD 5,400 per ounce in late January 2026 before giving back much of these gains. Our gold coverage is overvalued.

Copper, aluminium, and metallurgical coal prices are also around 10% higher on supply concerns, while the iron ore price is steady despite strong China imports.

Undervalued stocks in the Basic Materials sector

To see undervalued stocks in the basic materials sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX basic materials stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the basic materials sector currently trading at a 4- or 5- star rating.

Communication Services

Telecoms have started the year on a strong footing as investors seek a safe haven from geopolitical uncertainty and growing fears of AI disruption. Increasing broadband competition from the rise of the "challengers" looks set to continue, with the incumbents losing about 20% market share since 2020. Given the commoditised nature of broadband, we expect further consolidation and acquisitions.

Another growing trend is the growth of mobile virtual network operators or, MVNOs. While the market share of MVNOs is relatively low in Australia at about 20%, they account for 40% market share in Europe. We expect incumbent telecoms to withstand these industry shifts, given broadband accounts for a small portion of their earnings and many operate their own MVNO subsidiaries.

In media, while there are undeniable structural pressures, we believe most media names are fundamentally cheap. Worsening advertising conditions will force further cost-cutting, and we expect more consolidation.

Whether traditional media can monetize their growing digital viewership while keeping a lid on programming costs and reducing headcount using technology remains to be seen. However, considering the rock-bottom valuations of around 4 to 5 times our forecast EBITDA, little needs to go right to see a meaningful improvement in share prices.

Undervalued stocks in the Communication Services sector

To see undervalued stocks in the communication services sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX communication services stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the communication services sector currently trading at a 4- or 5- star rating.

Consumer Cyclical

Fuel prices have risen sharply since the Iran war began, weighing on household budgets. A prolonged period of elevated fuel prices would deliver a heavy blow to consumers, and we expect the impact on consumption would be higher than the Reserve Bank’s current tightening cycle. Discretionary categories appear set to wear the brunt of the downturn as consumers prioritize essentials, like groceries.

But we expect the impact to be temporary, and the bounce-back to be significant once hostilities end, bringing consumption back to long-term trends. Any weakness in demand for durable goods is likely to be caught up once oil prices ease.

Despite oil shock-induced inflationary pressures on discretionary spending, households could opt to materially reduce their savings to hold up their living standards, as they did in the post-pandemic cost-of-living crisis. We estimate the savings rate has since recovered, now at 7%, from most recent lows of 2% in 2023.

“Time to buy a major household item” is at its lowest since pandemic lockdowns began. Consumer sentiment was already weakening before the Iran war. But now the ANZ-Roy Morgan Australian consumer confidence index is at the lowest level since records began in 1973.

Undervalued stocks in the Consumer Cyclical sector

To see undervalued stocks in the consumer cyclical sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX consumer cyclical stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the consumer cyclical sector currently trading at a 4- or 5- star rating.

Consumer Defensive

Relatively inelastic demand for nondiscretionary goods and services means defensive retailers are more sheltered from a real spending squeeze. We expect lower overall consumption would mostly hit durable goods retailing, with demand for food and liquor to remain robust.

Inflation supports food retail industry sales growth, potentially creating a near-term boost for supermarkets. We expect to see major supermarket chains increase prices in response to rising inputs costs. But inflation could be a lingering issue if inflation expectations remain elevated and the wage bill catches up. Indeed, inflation expectations are highest since the ANZ-Roy Morgan consumer survey began tracking them in 2010.

Supermarkets are notoriously slow to respond to increased supplier costs. These suppliers are reliant on supermarkets and typically have difficulty raising prices to completely offset rising input costs such as feed, milk, fertiliser, and labour. Nevertheless, we expect supplier margins to gradually recover as cost pressures abate, cost efficiencies are won, and lagged price increases take effect.

Liquor could see trading down to cheaper, lower-margin beverages—and potentially trading down from pubs to at-home consumption.

Undervalued stocks in the Consumer Defensive sector

To see undervalued stocks in the consumer defensive sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX consumer defensive stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the consumer defensive sector currently trading at a 4- or 5- star rating.

Healthcare

We view the healthcare sector as undervalued on average, with over three-quarters of our coverage trading in 4- or 5-star territory.

The February reporting season was eventful, triggering large share price moves for many companies. We changed our fair value estimates for 10 healthcare names, with an average decrease of 4%.

Industry wage inflation is stabilising at a lower level. We expect wage growth to gradually ease on better staff availability from government initiatives, utilisation, and reduced agency staff, supporting margin expansion for operators.

Undervalued stocks in the Healthcare sector

To see undervalued stocks in the healthcare sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX healthcare stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the healthcare sector currently trading at a 4- or 5- star rating.

Industrials

Rising oil prices from the war in the Middle East is likely to push inflation further above targets in Australia and the US. If the central banks raise interest rates to bring inflation into line, this is likely to prolong cyclical weakness for our industrial coverage.

The war means uncertainty skews to the downside, but for now, we still expect a recovery through 2027. This is driven by an undersupply of houses in Australia and our expectation for the US federal-funds rate to fall by about 80 basis points in 2027. We believe building product and packaging companies have reached a cyclical trough and are awaiting a recovery.

The fuel bill is typically 20%–25% of an airline’s revenue, and short-term fluctuations can vaporize profits. We expect profit pressure in the near term. Fuel costs have surged too quickly for higher ticket prices to meaningfully offset. But long-term profitability has little to do with fuel, given all players bear the cost almost equally and costs are passed through to consumers in higher ticket prices.

Undervalued stocks in the Industrials sector

To see undervalued stocks in the industrials sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX industrial stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the industrials sector currently trading at a 4- or 5- star rating.

Real Estate

Investor sentiment flipped like a switch, as the Reserve Bank of Australia U-turned and delivered two 25-basis-point rate hikes in February and March, respectively. The recent conflict in the Middle East exacerbates the inflation outlook, with more than half the market now expecting a follow-up rate rise in May. Rising interest rates hurt real estate prices. In the March quarter, it massively underperformed the broader index, with the sector now trading roughly 20% below fair value estimates on average.

The February reporting season was relatively benign. We made no major fair value changes.

The worry around artificial intelligence-driven mass unemployment permeated the office pricing at the start of 2026. AI adoption could wipe out many white-collar jobs, reducing office space needs. At this stage, however, it is unclear how many jobs will get displaced by AI and how many new roles will be created, let alone the impact on office demand. That said, not all offices are created equal, and well-located high-quality buildings with modern amenities and high sustainability standards are best positioned to retain tenants, if there are declines in the number of office jobs. Office continues to show signs of improvement in the six months to December 2025, especially in city centres. Occupancy across major landlords held largely steady.

Undervalued stocks in the Real Estate sector

To see undervalued stocks in the real estate sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX real estate stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the real estate sector currently trading at a 4- or 5- star rating.

Utilities

Australian utilities screen as slightly undervalued on average. The Iran war has reduced global oil and LNG supply by about 20%, putting upward pressure on energy prices, including coal and gas.

Australian electricity futures prices have risen more than 10% as higher fuel costs are factored in. While not our base case, prices could go a lot higher if Middle East issues aren’t resolved quickly, especially if Australia runs out of diesel for mining and transport.

Undervalued stocks in the Utilities sector

To see undervalued stocks in the utilities sector, sign up for a FREE 4-week trial^ of Morningstar Investor (no credit card needed) to access all our latest best ASX utilities stock picks inside our ‘Australian Equity Market Outlook Q2 2026’ Your Money Weekly issue, plus our premium stock screener that will help you identify all stocks in the utilities sector currently trading at a 4- or 5- star rating.

Looking for more stock ideas?

The Morningstar Rating for shares can help investors uncover stocks that are truly undervalued, cutting through the market noise.

Investors can turn to several metrics to gauge a stock’s worth. Some investors use standard metrics, such as price/earnings or price/cash flows. Others may look at a stock’s price relative to a company’s future growth prospects, or where a stock is trading relative to its 52-week high price.

At Morningstar, we define undervalued stocks as those that are trading below our calculated fair value estimate, adjusted for what we call uncertainty—both of which are wrapped into the Morningstar Rating for stocks. Stocks rated 4 and 5 stars are undervalued; those rated 3 stars are fairly valued, and those rated 1 or 2 stars are overvalued.

To see our current 5-star rated stocks and best ideas, or screen our database of over 46,000 ASX & Global companies, sign up for a FREE 4-week trial^ of Morningstar Investor.

5-star Australian shares

Global equity best ideas

Australian stocks with moats

Inexpensive growth

Sustainable income

Inexpensive quality

5-star North American shares

5-star Asian stocks

About Us

It started with an idea—one great idea from a 27-year-old stock analyst. Joe Mansueto thought it was unfair that people didn’t have access to the same information as financial professionals. So he hired a few people and set up shop in his apartment—to deliver investment research to everyone. We didn’t know then what the company would look like today, but we knew the commitment to our mission—to empower investor success—wouldn’t change. Now, we operate through wholly- or majority-owned subsidiaries in over 30 countries. We’ve empowered investors all over the world, and we’re continuing to look for new ways to help people achieve financial security.

For over 40 years, that mission has remained the same — we believe in the democratisation of investment information, research, and data. It's at the core of everything we do.